Extras din curs

Societatea A absoarbe societatea B in conditiile in care cele doua societati participante la aceasta operatiune sunt independete din punct de vedere al participatiilor la capitalul social. Bilanturile contabile ale celor doua societati se prezinta astfel:

Elemente de activ A B Elemente de pasiv A B

Intangible assets 5.000 10.000 Social capital 50.000 75.000

Tangible assets 100.000 75.000 Provisons 25.000 5.000

Commodities 45.000 35.000 Retained earning 40.000 10.000

Clients 80.000 45.000 Suppliers 70.000 40.000

Treasury 40.000 55.000 Bank loans for long term 85.000 90.000

Total assets 270.000 220.000 Total liabilities 270.000 220.000

At historical cost we add:

a. Goodwill for A: 90.000 lei; and for B: 70.000 lei.

b. Plus value resulted by assesment of tangible assets for A: 40.000 lei; for B: 30.000 lei.

1) the mergers base - corrected net asset

Elemente A B

Owner Equity 115.000 90.000

- fictiv assets ( intangible assets) -5.000 -10.000

+ goodwill 90.000 70.000

+ Plus values 40.000 30.000

90.000

Corrected net active (ANC) 240.000 180.000

Shares nr = social cap/ nominal value (Na) 10.000 15.000

Actual value of shares (ANC/Na) 24 12

Nominal value of shares for A and B is 5 lei.

2) actual value of shares for A is 24 and for B is 12

3) Exchange rate between A and B actual values of shares: 24 A -----12 B 2A for 1 B Er = 2A/1B of 1B/2A

4) Nr of shares which will be issues by A NrA = QEB /AVA = 180.000/24= 7.500

Another formula to calculate Nr A = Er x Shares B = ½ x 15.000 = 7.500

5) Increasing the social capital of A ISC = Nr A x NV A = 7.500 shares x 5 = 37.500 lei;

6) mergers difference Md = OE B - ISC Md = 180.000 – 37.500 = 142.500

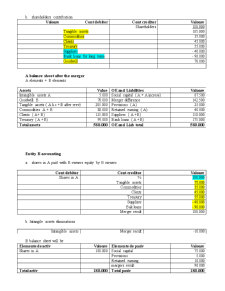

Entity A accounting

a. increse of social capital A

Cont debitor Cont creditor Valoare

Shareholders /.

Social capital

Merger difference 180.000

37.500

142.500

b. shareholders contribution

Valoare Cont debitor Cont creditor Valoare

Tangible assets Shareholders 180.000

105.000

Commodities 35.000

Clients 45.000

Treasury 55.000

Suppliers - 40.000

Bank loans for long term - 90.000

Goodwill 70.000

A balance sheet after the merger

A elements + B elements

Assets Value OE and Liabilities Valoare

Intangible assets A 5.000 Social capital ( A + A increse) 87.500

Goodwill B 70.000 Merger difference 142.500

Tangible assets ( A h.c +B after reev) 205.000 Provisions ( A) 25.000

Commodities A + B 80.000 Retained earning ( A) 40.000

Clients ( A+ B) 125.000 Suppliers ( A +B) 110.000

Treasury ( A +B) 95.000 Bank loans ( A +B) 175.000

Total assets 580.000 OE and Liab total 580.000

Entity B accounting

a. shares in A paid with B owners equity by B owners

Cont debitor Cont creditor Valoare

Shares in A % 180.000

Tangible assets 75.000

Commodities 35.000

Clents 45.000

Treasury 55.000

Suppliers - 40.000

Bak loans - 90.000

Merger result 100.000

b. Intangile assets eliminations

Intangible assets Merger result -10.000

B balance sheet will be

Elemente de activ Valoare Elemente de pasiv Valoare

Shares in A 180.000 Social capital 75.000

Provisions 5.000

Retained earning 10.000

mergers result 90.000

Total activ 180.000 Total pasiv 180.000

b. closing the entity B- the shareholders B right to receive them owner equity value

Cont debitor Cont creditor Valoare

./.

Social capital

Provisions

Retained earnings

Merger result Shareholders B 180.000

75.000

5.000

10.000

90.000

c. the shareholders B receives the owner equity value in A shares

Cont debitor Cont creditor Valoare

Sharehoders B Shares A 180.000

Preview document

Conținut arhivă zip

- Fuziuni

- Fuziune1.doc

- Fuziune2.doc

- Fuziune3.doc

- Fuziune4.doc

- Fuziune5.doc

Alții au mai descărcat și

CAPITOLUL 1 ANALIZA DIAGNOSTIC – DOMENIU DE STUDIU ŞI ACTIVITATE PROFESIONALĂ ÎN CADRUL UNEI ÎNTREPRINDERI 1.1. Introducere în problematica...

Cap.1. ORGANIZAREA ŞI STRUCTURA RESTAURANTELOR Serviciile de cazare şi alimentaţie au un rol distinct, esenţial şi primordial în ansamblul...

DEFINIŢII Conform Institutului de Marketing, marketingul este “procesul managerial responsabil de identificarea, anticiparea şi satisfacerea...

1 Factorii de productie La baza oricarei activitati economice , se afla resursele economice Resursele economice Reprezinta totalitatea...

Tema 1: Conceptul, esenţa şi rolul preţurilor în economie 1.1 Abordarea conceptului de preţ în teoria economică 1.2 Funcţiile preţului 1.3...

1. Tipuri de derivate financiare Derivatele financiare, parte integrantă a mediului investiţional, ce răspund necesităţilor operatorilor în...

1.1. Esenţa şi rolul finanţelor întreprinderii Teoria financiară se împarte în 3 compartimente mari: 1. Finanţe publice – studiază modul de...

Te-ar putea interesa și

Introducere Evoluţia fuziunilor în România În ultimii ani, progresele notabile făcute de ţara noastră, din punct de vedere al performanţelor...

INTRODUCERE Fuziunea societăţilor comerciale reprezintă o necesitate în Uniunea Europeană. Pentru a face faţă concurenţei si mai ales pentru a nu...

INTRODUCERE Fuziunea societăţilor comerciale reprezintă o necesitate în Uniunea Europeană. Pentru a face faţă concurenţei si mai ales pentru a nu...

FUZIUNEA SOCIETATILOR COMERIALE 1) CONCEPT – DELIMITARI SI REFERINTE Fuziunea este operatia prin care patrimoniul unei societati este transmis...

Concept – delimitari si referinte Din punct de vedere juridic, operatiunile de fuziune si divizare sunt reglementate prin Legea nr. 31/1990,...

Capitolul 1 Metoda rezultatului, respectiv evaluarea globala a societatilor Din punct de vedere juridic, operatiunile de fuziune si divizare sunt...

Din punct de vedere tehnic, fuziunea consta în combinarea a doua sau mai multe companii cu scopul de a crea o entitate economica prin unificarea...

INTRODUCERE Odată cu trecerea la economia de piaţă, activitatea societăţilor comerciale s-a diversificat foarte mult. În consecinţă, pe lângă...